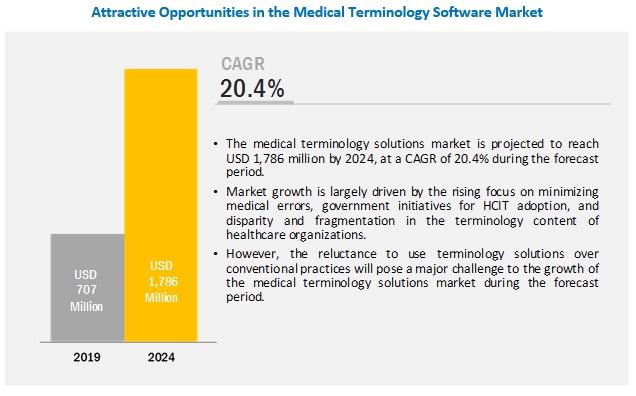

The growth in this market is driven by factors such as the rising focus on minimizing medical errors, government initiatives for HCIT adoption, and disparity and fragmentation in the terminology content of healthcare organizations.

The large share of this segment can be attributed to the growing focus on reducing medical errors and the need to create a consistent and comprehensive data source and improve performance measurement and transparency in patient care.

The large share of this segment can be attributed to the increasing demand for the standardization of patient data and the rising need to curb medical errors and accumulation of large amounts of healthcare data.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=239939409

The large share of North America is attributed to the high adoption of HCIT technologies, regulatory requirements regarding patient safety, the presence of leading market players in the region, and growing demand for accurate data exchange between healthcare providers and payers to streamline workflows.

Prominent players in the medical terminology software market are Wolters Kluwer (Netherlands), Intelligent Medical Objects (US), Apelon (US), Clinical Architecture (US), 3M (US), CareCom (Denmark), Bitac (Spain), B2i Healthcare (Hungary), BT Clinical Computing (Belgium), and HiveWorx (Ireland).