Topical, oral, and parenteral pain medications are widely used to manage pain associated with osteoarthritis. Although alternatives such as orthopedic braces are used as part of a noninvasive approach for pain management, the adoption of pain medications for the condition is high owing to the ease of administration and the affordability of pain medications. Pain relievers such as oral analgesics (acetaminophen and NSAIDs such as ibuprofen, naproxen, tramadol, opiates, and duloxetine), topical agents (such as capsaicin and topical NSAIDs), intra-articular agents (such as corticosteroids and hyaluronic acid), and nutraceuticals (glucosamine and chondroitin) are widely used. Studies reveal that these medications offer a 30% reduction of chronic pain on administration.

The adoption of pain medications for the management of pain associated with osteoarthritis is expected to remain high over the coming decade, which is anticipated to propel the growth of the market during the study period.

OTC and prescription NSAIDs are widely used to relieve pain in osteoarthritis patients. As per a study published by the National Center for Biotechnology Information in 2019, more than 50% of osteoarthritis patients in the US are prescribed NSAIDs. Similarly, in Europe, of the total number of osteoarthritis patients using prescription medications (47%), 60% received NSAIDs.

The use of NSAIDs is associated with an increased risk of adverse cardiovascular events. Both cyclooxygenase (COX)-2 selective NSAIDs (coxibs) and non-selective NSAIDs increase CVD risk in patients. A study presented at the Annual European Congress of Rheumatology (EULAR 2018) stated that more than two-thirds of the increased cardiovascular risk associated with osteoarthritis is linked to NSAIDs. Such risks associated with the use of NSAIDs can potentially discourage doctors from prescribing these medications while driving patients using OTC NSAIDs to opt for alternative products.

For More Info, Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=209565994

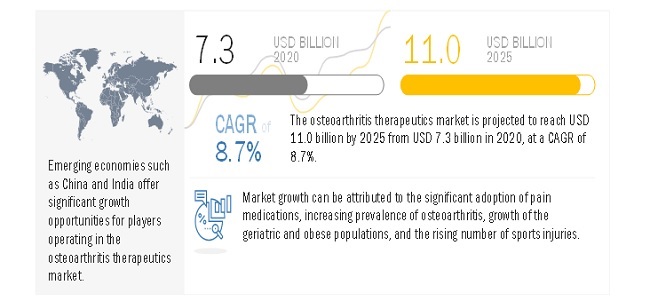

[201 Pages Report] The osteoarthritis therapeutics market is projected to reach USD 11.0 billion by 2025 from USD 7.3 billion in 2020, at a CAGR of 8.7% from 2020 to 2025. The presence of a large geriatric and target patient population and the improving healthcare infrastructure in several APAC countries are expected to offer growth opportunities in the market during the forecast period.

Remarkable advances have been made in diagnosing, treating, and monitoring disease activity in patients with osteoarthritis, including the conceptualization of personalized OA medications. Essential features of biomarkers that will have clinical relevance for a personalized approach to therapy for RA include the ease of measurement, acceptable levels of sensitivity and specificity, and test methods that are accessible and interpretable by clinicians.

The use of biomarkers to identify patients who are likely to respond to specific medical therapies may increase treatment response rates and reduce the risk of exposure to therapies that are unlikely to be effective or expose patients to serious treatment-related side-effects. The combination of unique biomarkers and baseline clinical characteristics such as sex and age may further enhance efforts to personalize treatment regimens for RA.

The analgesics segment is subsegmented into duloxetine and acetaminophen, while the NSAIDs segment is subsegmented into naproxen, aspirin, diclofenac, ibuprofen, and other NSAIDs. The viscosupplementation agents segment accounted for the largest share of the osteoarthritis therapeutics market in 2019. The rising incidence of knee osteoarthritis is the major factor driving the growth of this segment. Viscosupplementation effectively eases the pain of osteoarthritis through injections that fill up the joint’s synovial fluid, thus offering better lubrication of the joints.

On the basis of region, the osteoarthritis therapeutics market is segmented into North America, Europe, Asia Pacific, and the Rest of the World. In 2019, Europe commanded the largest share of the osteoarthritis therapeutics market. The large share of this market segment can be attributed to the rising incidence of osteoarthritis, rising geriatric population, and increasing obesity rates in several European countries, coupled with the rising number of injuries due to sports and road accidents.