Traumatic and surgical wounds segment accounted for the largest share of the biofilms treatment market in 2019.

Based on the wound type, the biofilms treatment market is segmented into surgical and traumatic wounds, diabetic foot ulcers, pressure ulcers, venous leg ulcers, and burns and other open wounds. The surgical and traumatic wounds segment accounted for the largest market share in 2019. The large share of this segment can be attributed to the growing prevalence of diabetes and the increasing number of surgical procedures performed.

Gauzes and dressings segment to witness the highest growth rate during the forecast period

Based on product, the biofilms treatment market is segmented into debridement equipment; gauzes and dressings; gels, ointments, and sprays; wipes, pads, and lavage solutions; and grafts and matrices. The gauzes and dressings segment accounted for the largest market share in 2019. The large share of this segment is attributed to the ability of antimicrobial products to remove, prevent, and manage biofilms.

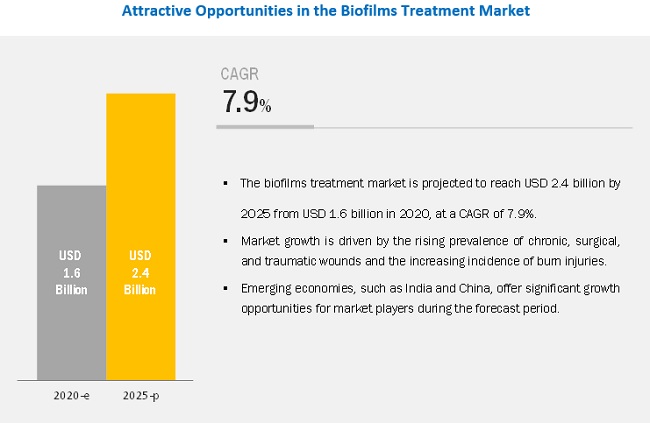

The biofilms treatment market is projected to reach USD 2.4 billion by 2025 from USD 1.6 billion in 2020, at a CAGR of 7.9%. Market growth is driven by the rising prevalence of chronic, surgical, and traumatic wounds and the increasing incidence of burn injuries.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=57398610

North America is the largest regional market for biofilms treatment

On the basis of region, the biofilms treatment market is segmented into North America, Europe, the Asia Pacific (APAC), Latin America (LATAM), and the Middle East & Africa (MEA). In 2019, North America accounted for the largest share of the biofilms treatment market. The large share of this market can be attributed to the increasing incidence of chronic wounds, rising healthcare expenditure, the introduction of novel and specialty biofilm management products, and the presence of major market players in this region.

Prominent players in the biofilms treatment market include Smith & Nephew (UK), MiMedx Group Inc. (US), ConvaTec Group plc (UK), Coloplast A/S (Denmark), Mölnlycke Healthcare AB (Sweden), Organogenesis Holdings Inc. (US), Integra LifeSciences Holdings Corporation (US), B. Braun Melsungen AG (Germany), PAUL HARTMANN AG (Germany), Medline Industries Inc. (US), Acelity (US), Misonix (US), Zimmer Biomet Holdings Inc. (US), Kerecis (Iceland), Welcare Industries S.p.A (Italy), Medaxis AG (Switzerland), PulseCare Medical (US), Arobella Medical, LLC (UK), RLS Global AB (Sweden), Mil Laboratories Pvt. Ltd. (India).