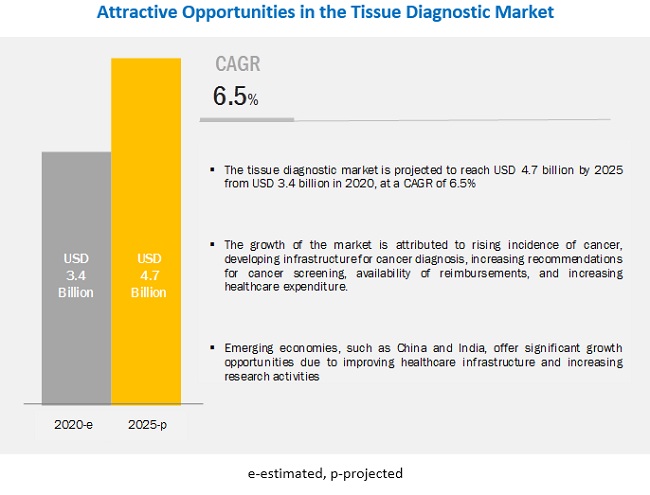

The global tissue diagnostic market size is expected to reach USD 4.7 billion by 2025 from USD 3.4 billion in 2020, at a CAGR of 6.5%. This industry is experiencing significant growth due to the rising incidence of cancer, developing infrastructure for cancer diagnosis, recommendation of cancer screening, availability of reimbursements, and increasing healthcare expenditure.

The consumables segment is expected to grow at the highest growth rate during the forecast period. This is attributed primarily to their requirement in large numbers, cost-effectiveness, and ease of use. The increasing number of reagent rental agreement is also one of the major factors to drive the growth of the consumables market globally.

The immunohistochemistry segment is estimated to register the highest CAGR during the forecast period. This can primarily be attributed to the increasing prevalence of chronic diseases across the globe, where this technology is mostly used in tissue diagnostics.

Easy accessibility to advanced technologies, government initiatives for screening cancer patients, favourable reimbursement scenario for pathology diagnostic tests, increasing healthcare expenditure, and high-quality infrastructure for hospitals and clinical laboratories in this region are the major factors driving the growth of the tissue diagnostic market in North America.

Key Market Players

The prominent players operating in the tissue diagnostic market include Roche (Switzerland), Danaher (US), Thermo Fisher Scientific (US), Abbott (US), Agilent Technologies (US), ABCAM (UK), Merck KGAA (Germany), BD (US), Hologic (US), Bio Rad (US), Biomeriux (France), Sakura Fientek Japan (Japan), BioSB (US), Biogenex (US), Cell Signaling Technology (US), Histoline Laboratories (Italy), Slee Medical GMBH (Germany), Amos Scientific PTY Ltd (Australia), Jinhua Yidi Medical Appliance Co.Ltd (China), Medite GMBH (Germany), Cellpath Ltd(UK), and Dipath S.P.A. (Italy).

Consumables accounted for the largest share of the tissue diagnostic market, by product, in 2019

By product, the tissue diagnostic market is segmented into instruments and consumables. The consumables segment is expected to grow at the highest rate during the forecast period. The large market share of this segment is attributed to their requirement in large numbers, cost-effectiveness, and ease of use. The increasing number of reagent rental agreements is also one of the major factors driving the growth of the consumables market.

By technology, immunohistochemistry accounted for the largest market share in 2019

Based on the technology, the tissue diagnostic market is segmented into immunohistochemistry, in situ hybridization, digital pathology and workflow, and special staining.

Get Data as per your Format and Definition | REQUEST FOR CUSTOMIZATION: https://www.marketsandmarkets.com/requestCustomizationNew.asp?id=1063949

The immunohistochemistry segment is estimated to register the highest CAGR during the forecast period. This can primarily be attributed to is increasing prevalence of chronic diseases across the globe, where this technology is mostly used in tissue diagnostics.

By disease, the breast segment accounted for the largest market share in 2019

By disease, the market is categorized into breast cancer, gastric cancer, lymphoma, prostate cancer, NSCLC, and other diseases. The breast cancer segment is expected to grow at the highest rate during the forecast period. The rising incidence of breast cancer is the major driving factor of this segment.

Hospitals accounted for the largest share of the tissue diagnostic market, by end user, in 2019

The end user segment of this market is categorized into hospitals, pharmaceutical companies, research laboratories, contract research organizations, and other end users. The research laboratories segment is expected to grow at the highest growth rate during the forecast period.

This can be attributed to increasing outpatient surgeries such as endoscopies performed in ambulatory surgical centers (ASCs) and physician offices, which has increased the number of samples outsourced to clinical laboratories. In addition, research laboratories also offer advantages such as excellent complex and specialized testing capabilities, efficient billing and collection systems, and low test costs.